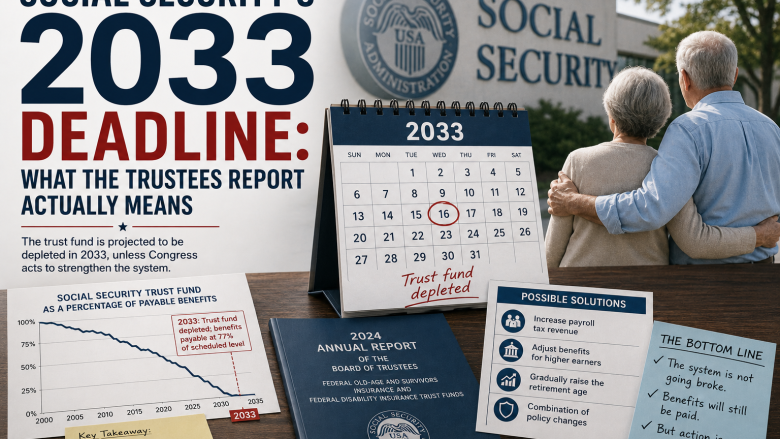

Every year, the Social Security and Medicare Boards of Trustees publish an annual report on the long-term financial status of the programs. Every year, the projections make headlines, generate alarm, and then are largely forgotten by a political system that has demonstrated little appetite for the difficult decisions the math requires. The 2026 Trustees Report, released in April, projects that the combined Social Security trust funds — Old-Age and Survivors Insurance (OASI) and Disability Insurance (DI) — will be exhausted by 2033. That is seven years from now. And the consequences of reaching that date without legislative action would be severe.

What Exhaustion Actually Means

The most important thing to understand about trust fund exhaustion is what it does and does not mean. Social Security is a pay-as-you-go system: current workers pay payroll taxes that fund current retirees’ benefits. The trust funds exist as a buffer — they were built up during the demographic sweet spot of the late 20th century, when the ratio of workers to retirees was favorable, and were always intended to be drawn down as baby boomers retired.

When the trust funds are exhausted, Social Security does not disappear. Tax revenue continues to flow in, and the program can continue to pay benefits — but only at the level that incoming revenue supports. The 2026 Trustees Report estimates that at the point of trust fund exhaustion in 2033, incoming revenue would cover approximately 79% of scheduled benefits. That means an automatic across-the-board benefit cut of approximately 21% would take effect — affecting not just new retirees, but everyone currently receiving Social Security.

For the average retired worker receiving $1,907 per month in Social Security benefits as of January 2026 (per the Social Security Administration’s most recent data), a 21% cut would reduce monthly income by approximately $400. For the roughly 25% of retirees for whom Social Security represents 90% or more of their income, this would be devastating. For the 62 million Americans currently receiving Social Security benefits of any kind, it would represent an abrupt and painful reduction in financial security.

The Demographic Driver

The financial stress facing Social Security is ultimately a demographic problem. The program was designed at a time when the ratio of workers to retirees was approximately 16 to 1. Today it stands at approximately 2.7 to 1, and by 2033 it is projected to decline further toward 2.3 to 1. Each worker’s payroll taxes must support a larger share of retiree benefits, and the math becomes increasingly challenging.

The baby boom — the enormous cohort born between 1946 and 1964 — is moving fully into retirement during exactly this period. Approximately 10,000 baby boomers are reaching age 65 every day, a rate that will continue through the late 2020s. Life expectancy has also extended significantly since the program was designed: a man reaching age 65 in 2026 can expect to live an average of 17.5 more years; a woman at 65 can expect 20.3 more years, according to the Social Security Administration’s period life table. In 1940, when the program paid its first benefits, life expectancy at 65 was just 12.7 years for men and 14.7 years for women.

The Options for Reform

The mathematics of Social Security solvency are not particularly complex, even if the politics are. The program can be made indefinitely solvent through some combination of increasing revenues, reducing benefits, raising the retirement age, adjusting the benefit formula, or changing cost-of-living adjustments. The Congressional Budget Office and Social Security Administration’s actuaries have modeled dozens of specific reform combinations and their effects on the program’s 75-year financial outlook.

On the revenue side, the most frequently discussed option is raising or eliminating the Social Security payroll tax cap. In 2026, workers pay 6.2% Social Security tax on wages up to $168,600 (the cap adjusts annually with wage growth). Wages above that amount are not subject to Social Security tax at all, meaning that high earners pay a smaller share of their income in Social Security taxes than middle-income workers do. Eliminating the cap entirely would, according to the CBO, close roughly 70% of the 75-year Social Security shortfall on its own.

On the benefit side, the most commonly discussed modification is raising the full retirement age. It currently stands at 67 for those born in 1960 or later, having been gradually increased from 65 under 1983 legislation. Raising it further to 68 or 69 would reduce lifetime benefit payments and improve the program’s finances, but would disproportionately affect workers in physically demanding jobs who may not be able to continue working until a higher retirement age.

The Political Stalemate

The reason Social Security has not been reformed despite the well-understood nature of its financial trajectory is straightforward: every available reform option creates losers who vote, and the political cost of loss aversion typically overwhelms the political benefit of responsible long-term governance.

Raising the payroll tax cap is opposed by high-income earners and the political figures who represent their interests. Raising the retirement age is opposed by unions and worker advocates concerned about its disparate impact on workers in physically demanding occupations. Reducing benefit growth is opposed by retirees and near-retirees who built financial plans around expected benefits. The coalition required to pass significant reform requires each political faction to accept some pain — and building that coalition has defeated every serious reform attempt for four decades.

The last significant Social Security reform was the bipartisan compromise of 1983, negotiated by Alan Greenspan’s commission and passed with the support of President Reagan and House Speaker Tip O’Neill. That reform included benefit cuts, revenue increases, and the phased increase in the retirement age — something for everyone to dislike, which was also the key to its success. Political observers who study Social Security policy largely agree that a similar grand bargain is the only realistic path to reform, and that it is unlikely to materialize until the trust fund depletion date is genuinely imminent.

What Individuals Should Know and Do

For individuals planning their retirement finances, the Social Security situation creates real uncertainty that must be factored into planning. The appropriate response is not to assume benefits will be zero — the program is not going away, and even under the worst-case scenario, 79 cents on the dollar is far better than nothing. But nor should younger workers assume that scheduled benefits will be paid in full.

Financial planners generally suggest using a 75-80% assumption for expected Social Security benefits in retirement planning for those more than 10 years from retirement, as a conservative buffer against the possibility of some benefit reduction. Workers in their 50s and early 60s have a stronger basis for expecting their full scheduled benefits, given the political reality that reform packages invariably include grandfather provisions protecting near-retirees from significant benefit changes.

The deeper lesson of the Social Security funding situation is that the US needs a more robust culture of private retirement saving to complement a program that was never intended — and cannot afford — to be the sole source of retirement income. The data on this point is sobering: the Federal Reserve’s Survey of Consumer Finances found that the median working-age household has saved just $87,000 for retirement — a figure that would sustain approximately 3-4 years of average retirement spending before being exhausted.

Sources: Social Security and Medicare Boards of Trustees 2026 Annual Report, Social Security Administration, Congressional Budget Office, Federal Reserve Survey of Consumer Finances