Few economic narratives have captured more political attention over the past decade than the promise of bringing manufacturing back to America. Presidents of both parties have made reshoring the cornerstone of their economic platforms, and the legislative output — the CHIPS Act, the Inflation Reduction Act, the Infrastructure Investment and Jobs Act — has been substantial. But as 2026 unfolds, it is worth asking an honest question: Is the US manufacturing renaissance a real economic transformation, or an expensive and incomplete policy aspiration being oversold by partisans on both sides?

The Investment Numbers Are Real

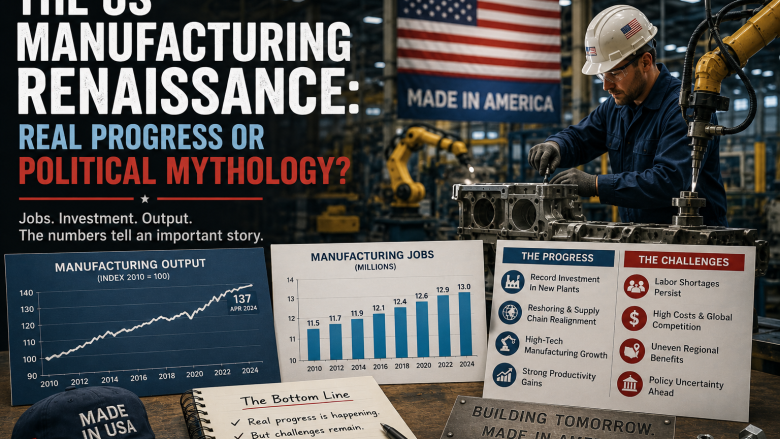

Let’s start with what is genuinely happening. Manufacturing construction spending in the United States has experienced an extraordinary acceleration. According to the Census Bureau’s Construction Spending survey, manufacturing construction put in place reached an annualized rate of $234 billion in Q1 2026 — more than double the level of Q1 2022 and the highest in records going back to 1993, adjusted for inflation.

The semiconductor sector accounts for a substantial portion of this surge. TSMC’s $65 billion Arizona fab complex is under construction, with the first plant having begun production of 4-nanometer chips in early 2025. Intel’s $20 billion Ohio campus broke ground in 2022 and is progressing toward its target opening. Samsung is building a $17 billion facility in Taylor, Texas. In aggregate, the CHIPS and Science Act has catalyzed announced US semiconductor manufacturing investment exceeding $400 billion since its passage, according to the Semiconductor Industry Association.

Electric vehicle and battery manufacturing has similarly seen dramatic investment announcements. Ford, GM, Toyota, Volkswagen, and dozens of battery cell manufacturers have announced US manufacturing facilities totaling hundreds of billions in planned investment, drawn by the IRA’s domestic content requirements that make US-manufactured EVs eligible for consumer tax credits that imported vehicles cannot access.

The Employment Reality Is More Complicated

Where the manufacturing renaissance narrative becomes more complicated is in the employment data. Manufacturing payrolls stood at 12.8 million in April 2026, essentially flat with the 12.9 million employed in the sector in January 2022 and still significantly below the 14 million employed in 2007 before the financial crisis. Despite the massive capital investment flowing into the sector, manufacturing employment has not recovered to its pre-Great Recession levels, let alone its peak of approximately 19 million in the late 1970s.

The explanation lies in the nature of modern manufacturing. The semiconductor fabs being built in Arizona and Ohio are highly capital-intensive facilities that employ far fewer workers per dollar of output than the factories they are intended to replace. A cutting-edge TSMC fab might employ 2,000-3,000 workers and require billions in equipment investment — producing enormous economic value but not restoring the broad-based blue-collar employment that characterized American manufacturing in its mid-20th century peak.

The Bureau of Labor Statistics data shows that manufacturing productivity has increased approximately 85% since 2000, meaning that today’s factories produce significantly more output per worker than they did a generation ago. This is economically beneficial — higher productivity supports higher wages for workers who remain in the sector — but it limits the extent to which even large capital investment translates into large-scale job creation.

The Skills Gap Challenge

A structural obstacle that policy cannot easily resolve is the shortage of workers with the skills that advanced manufacturing requires. The Deloitte and Manufacturing Institute’s 2026 skills gap report estimated that the manufacturing sector will need to fill 3.8 million jobs over the next 10 years, but that roughly 1.9 million of those positions may go unfilled due to the skills gap — the mismatch between available workers and required capabilities.

Semiconductor manufacturing, in particular, requires a workforce pipeline of engineers, technicians, and skilled tradespeople that the US higher education and vocational training systems have not historically been oriented to produce in sufficient quantities. The CHIPS Act included $13.2 billion specifically for workforce development and education, but building the human capital pipeline for advanced manufacturing takes years — potentially longer than the facilities themselves take to construct.

TSMC has publicly struggled with this challenge at its Arizona facility, noting in 2023 that it was importing experienced engineers and technicians from Taiwan because it could not find sufficient skilled workers locally. The company subsequently committed to expanded partnerships with Arizona State University and community colleges, but the gap between the available workforce and the required workforce remains a bottleneck.

The Cost Competitiveness Question

American manufacturing is more expensive than production in most competitor countries, and honest assessment requires acknowledging the implications. The Peterson Institute for International Economics estimated that manufacturing semiconductors in the United States costs 30-50% more than equivalent production in Taiwan or South Korea, even accounting for CHIPS Act subsidies. Without those subsidies — which are necessarily time-limited and budget-constrained — the cost differential would be even larger.

For industries competing in global markets, this cost premium is a real competitive challenge. US manufacturers can compete on quality, proximity, and supply chain resilience — and there is genuine demand from customers willing to pay a premium for those attributes — but the market for “made in America” has limits that economic nationalism cannot overcome through political will alone.

The IRA’s domestic content requirements are effectively a subsidy that enables US EV manufacturers to offer competitive prices on vehicles that would otherwise be more expensive than their imported equivalents. This is a defensible policy choice from a national security and industrial strategy perspective, but it is ultimately a cost that is borne by taxpayers and, through higher prices, by consumers.

The Geographic Distribution of Benefits

One dimension of the manufacturing investment wave that deserves attention is its geographic distribution. The large-scale facilities being built are concentrated in specific states and regions: Ohio, Arizona, Texas, Georgia, Tennessee, and the Carolinas have attracted the largest investments, reflecting a combination of available land, lower-cost labor markets, business-friendly regulatory environments, and state-level incentives packages that have been substantial.

The Rust Belt communities that lost manufacturing employment in the 2000s and 2010s — communities in Pennsylvania, Michigan, Wisconsin, and Indiana — have received a smaller share of the new investment than political rhetoric might suggest. The new manufacturing economy is being built where conditions for advanced manufacturing are most favorable, which is not necessarily where the human cost of deindustrialization was most severe.

The Verdict: Real, But Partial

The honest answer to whether the US manufacturing renaissance is real is: yes, but not in the way that either its proponents or its critics often portray. The capital investment is genuine and substantial, and it will have real economic benefits in the form of supply chain resilience, reduced geopolitical vulnerability, and quality employment for skilled workers in the sectors receiving investment.

But it will not restore the broad-based manufacturing employment that characterized the mid-20th century American economy. It will not be cost-competitive without ongoing subsidy in many sectors. And it will not reverse the geographic dislocation that decades of manufacturing decline created in communities across the Midwest and South. What it can do — and is doing — is build the foundation for an advanced manufacturing sector suited to the 21st century rather than the 20th. That is a meaningful achievement, even if it is not the political narrative that either party prefers to tell.

Sources: Census Bureau, Semiconductor Industry Association, Bureau of Labor Statistics, Deloitte/Manufacturing Institute, Peterson Institute for International Economics, Federal Reserve