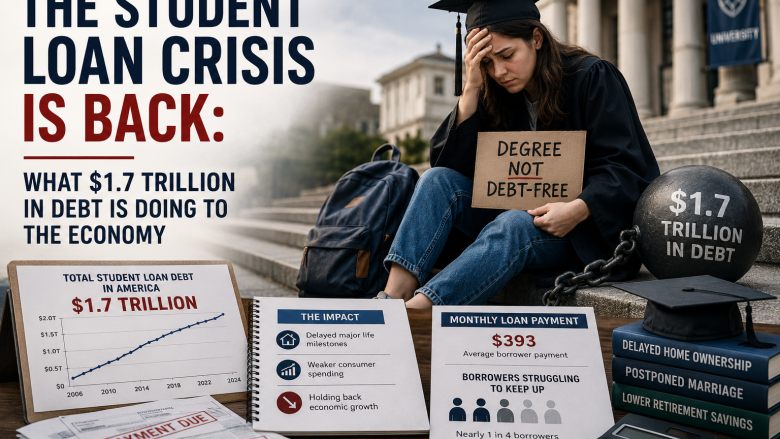

Student loan debt in the United States reached $1.77 trillion as of Q1 2026, according to the Federal Reserve’s Household Debt and Credit Report — a figure that has been climbing for decades and now represents the second-largest category of consumer debt after mortgages. But the story of student debt in 2026 is not just about the size of the number. It’s about what happened when repayments resumed after a multi-year pandemic pause, and what the data reveals about the impact of this debt burden on housing, retirement savings, family formation, and the broader economy.

The Repayment Resumption and Its Fallout

The federal student loan repayment moratorium, first implemented in March 2020, was extended repeatedly before finally ending in October 2023. The resumption of payments after more than three years — during which roughly 44 million borrowers had enjoyed zero-interest forbearance — was one of the most anticipated economic transitions of the past decade.

The Department of Education reported that as of December 2025, approximately 38% of borrowers with payments now due are in some form of delinquency or default — a figure substantially higher than the pre-pandemic default rate of approximately 10-11%. The New York Fed’s consumer finance researchers estimated that the resumption of student loan payments has reduced discretionary household spending by approximately $22 billion annually for affected households, a drag on consumer spending that has contributed to the retail sector’s softening.

The income-driven repayment plan restructuring attempted by the Biden administration — particularly the SAVE plan — was struck down by federal courts in 2025, leaving many borrowers in limbo about their actual monthly payment obligations. This legal uncertainty has compounded the confusion and financial stress already inherent in resuming payments after a 3.5-year pause.

Who Holds the Debt

Understanding the distributional reality of student debt is essential to assessing its economic impact. Despite popular perception, the student debt problem is not concentrated among the highest earners. Research from the Urban Institute using Federal Reserve data found that borrowers in the bottom income quintile are three times more likely to default on student loans than those in the top quintile, because higher-earning graduates tend to have degrees from institutions with strong earnings outcomes that justify the debt burden.

The highest-risk borrowers are those who attended college but did not graduate — roughly 38% of borrowers who hold federal loans — and those who attended for-profit institutions that have since faced regulatory scrutiny or closure. For these borrowers, the debt burden can be substantial while the credential-based earnings premium that was supposed to justify it never materialized.

Graduate professional debt is concentrated differently. Law school graduates typically carry $130,000-$180,000 in debt; medical school graduates average $250,000 or more. These borrowers tend to have higher earnings and better ability to service their debt, but the sheer scale of the obligation shapes their financial decisions for the first decade of their careers in ways that affect savings rates, home purchases, and family formation timing.

The Housing Market Impact

Perhaps the most economically significant consequence of the student debt burden is its contribution to homeownership delays among younger Americans. Research from the National Association of Realtors found that 51% of non-homeowning millennials cited student loan debt as a primary barrier to homeownership. The Federal Reserve Bank of Philadelphia estimated that each $1,000 increase in student loan debt reduces the probability of homeownership by approximately 1.8 percentage points for borrowers in their 30s.

When students graduate carrying $30,000-$50,000 in debt and spending $300-$500 per month on debt service, they simultaneously accumulate less for a down payment, qualify for a smaller mortgage (since student loan payments count against debt-to-income ratios in underwriting), and feel greater psychological reluctance to take on additional debt. The aggregate effect of this dynamic on homeownership rates among millennials is substantial and has contributed to the generationally low homeownership rates documented in the Harvard Joint Center’s most recent housing report.

The Retirement Savings Displacement Effect

A less visible but equally consequential impact of student debt is its displacement of retirement saving. The Employee Benefit Research Institute’s 2026 Retirement Confidence Survey found that 43% of student loan borrowers in their 20s and 30s are not contributing to employer-sponsored retirement plans — compared to 22% of non-borrowers in the same age cohort.

The compounding math of this divergence is severe. A 25-year-old who delays 401(k) contributions for 10 years to manage student debt loses not only those years of contributions but the compound growth that would have accumulated on them over a 40-year career. Vanguard’s research estimated that a borrower who delays retirement saving by 10 years will retire with approximately 40% less wealth than an otherwise identical saver who began at age 25, even if they contribute identical amounts from age 35 onward.

The For-Profit College Reckoning

A subset of the student debt crisis involves borrowers who attended institutions that are now viewed as having misrepresented their outcomes. The Department of Education’s Borrower Defense to Repayment program has processed approximately $19.7 billion in loan discharges for former students of institutions like ITT Technical Institute, Corinthian Colleges, and Art Institutes — for-profit chains that faced allegations of fraudulent recruiting practices and inflated employment outcome statistics.

The 2026 settlement with the Art Institutes chain, totaling $1.4 billion in debt relief for approximately 317,000 borrowers, was among the largest in the program’s history. While these discharges represent meaningful relief for affected borrowers, they also represent a significant cost to taxpayers who ultimately bear the loss when federal loans are discharged — a cost that has re-energized the debate about accountability standards for institutions receiving federal financial aid.

The Policy Landscape After the Supreme Court

The Supreme Court’s 2023 decision striking down President Biden’s broad student loan forgiveness plan foreclosed the most ambitious attempt at debt relief in the program’s history. Since then, targeted relief through program-specific mechanisms — Public Service Loan Forgiveness, Borrower Defense, Total and Permanent Disability discharge — has continued at a meaningful pace, with the Biden and subsequent administration discharging approximately $167 billion in student debt through these channels by early 2026.

The policy debate has shifted toward structural reforms rather than mass forgiveness: income-driven repayment that is simpler and more automatic, stronger institutional accountability measures tied to student outcomes data, and increased investment in community colleges and public university systems to reduce the debt burden for future borrowers. Whether these reforms achieve sufficient political support in 2026 and beyond remains to be seen.

What Borrowers Should Know Now

For borrowers navigating the current landscape, several practical realities apply. The income-driven repayment options that survive legal challenges can meaningfully reduce monthly payments for borrowers in lower-paying careers. Public Service Loan Forgiveness remains a viable pathway for those working in government, education, or qualifying nonprofit roles. Borrowers experiencing genuine financial hardship should contact their loan servicer immediately to explore deferment or forbearance options rather than allowing loans to enter default, which carries severe credit score consequences and can result in wage garnishment.

The student loan crisis is not a simple story of irresponsible borrowers. It is the product of a higher education financing system that shifted enormous costs onto students and families during a period when real wages stagnated and tuition costs significantly outpaced inflation. The data makes clear that the consequences of that shift are now rippling through the broader economy in ways that affect all Americans — not just those writing the monthly check.

Sources: Federal Reserve, Department of Education, New York Fed, Urban Institute, National Association of Realtors, Federal Reserve Bank of Philadelphia, Employee Benefit Research Institute, Harvard Joint Center for Housing Studies, Vanguard, Borrower Defense to Repayment program data