The American dream of homeownership is facing its most severe affordability crisis since the early 1980s. A combination of elevated mortgage rates, constrained housing supply, and home prices that never fully corrected from their pandemic-era surge has pushed housing affordability to generational lows — a reality that is reshaping household formation patterns, wealth accumulation, and the geographic distribution of economic opportunity across the United States.

The Affordability Index: What the Numbers Say

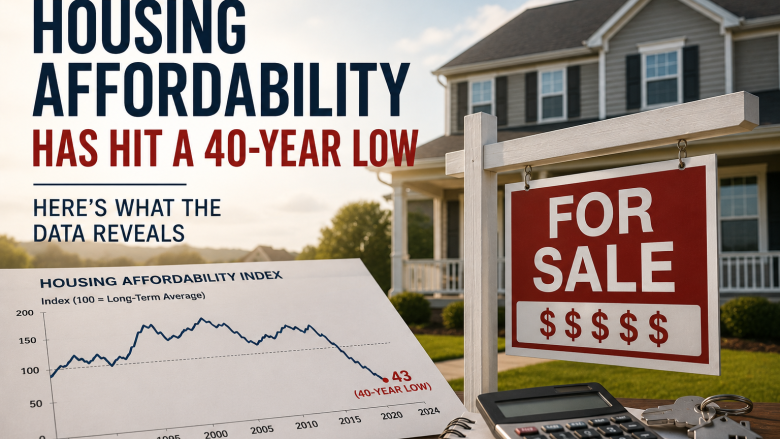

The National Association of Realtors’ Housing Affordability Index measures whether a typical family earning the median income can qualify for a mortgage on a median-priced home. A score of 100 means the family has exactly enough income to qualify. As of April 2026, the index stood at 92.4 — the lowest reading since 1985 and well below the long-run average of approximately 140.

To put this in concrete terms: the median US home price stands at approximately $432,000 as of Q1 2026, according to the Federal Reserve Bank of St. Louis. With a 30-year fixed mortgage rate of 7.1%, a buyer putting 10% down would face a monthly mortgage payment of roughly $2,870 — before property taxes, insurance, or HOA fees. The Bureau of Labor Statistics reports that median household income in the US is approximately $80,600. Standard lending guidelines suggest that total housing costs should not exceed 28-30% of gross income, which equates to a monthly limit of approximately $1,880-$2,015 for a median-income household. The math simply does not work for most buyers without significant assistance.

The Supply Shortage: A Decade in the Making

The affordability crisis cannot be fully understood without examining the supply side of the equation. The United States entered the 2020s with a significant housing deficit that had been building for over a decade. The National Association of Realtors estimated in its 2026 housing report that the country faces a shortfall of approximately 5.5 million homes relative to underlying demographic demand — a gap that reflects the dramatic underbuilding that followed the 2008 financial crisis.

Housing starts collapsed from a peak of 2.07 million annually in 2005 to just 554,000 in 2009, and the construction industry never fully recovered the skilled labor force or production capacity it had before the crisis. Even the building boom of 2020-2022 failed to close the gap, partly because it was concentrated in single-family homes in suburban and exurban areas rather than the affordable multifamily housing most needed in dense employment centers.

Zoning restrictions and NIMBYism compound the supply problem. A 2026 analysis by the Urban Institute found that 70% of residential land in major US metro areas is zoned exclusively for single-family housing, effectively prohibiting the higher-density development that could most efficiently address the shortage. Recent state-level preemption laws in California, Washington, and Montana have begun to challenge these restrictions, but the construction pipeline responds slowly to regulatory changes.

The Lock-In Effect: Why Existing Homeowners Won’t Sell

A structural feature of the current housing market that has no historical precedent is the “mortgage lock-in effect.” During 2020 and 2021, roughly 15 million US homeowners refinanced into mortgages with rates between 2.5% and 3.5%. Moving to a new home would require trading that sub-3% rate for a 7%+ rate on a new mortgage — an increase in monthly payments so dramatic that, for most homeowners, staying put is the overwhelming financial choice.

The Federal Housing Finance Agency estimated in a 2026 analysis that this lock-in effect is suppressing existing home sales by approximately 1.2 million units annually. Inventory of existing homes for sale stands at just 2.8 months’ supply as of May 2026, according to Realtor.com, far below the 5-6 months considered a balanced market. This inventory shortage is preventing home prices from falling even as affordability deteriorates — creating a market where sellers cannot afford to sell and buyers cannot afford to buy.

The Demographic Crunch

The timing of this affordability crisis is particularly cruel because it coincides with the peak homebuying years of the millennial generation. Americans born between 1981 and 1996 are now aged 30 to 45 — the cohort most likely to be forming families, earning their strongest salaries, and seeking to build wealth through homeownership. This is the largest generational cohort in American history, with approximately 72 million members.

The Harvard Joint Center for Housing Studies’ 2026 State of the Nation’s Housing report found that homeownership rates among adults aged 30-34 fell to 48.7% in 2025, down from 53.1% in 2000 and the lowest rate in records going back to the 1960s. For 25-29 year olds, the rate is just 34.2%. These rates matter enormously for wealth accumulation, because homeownership has historically been the primary mechanism through which middle-class families build intergenerational wealth in the United States.

Geographic Winners and Losers

Not all housing markets are equally unaffordable. Markets in the Midwest — particularly metro areas like Columbus, Indianapolis, Cleveland, and Kansas City — remain significantly more accessible than coastal metros. The NAR’s affordability data shows that in Columbus, Ohio, a median-income household can afford a median-priced home; the same household in San Francisco would need to earn 4.1 times the median income to qualify.

This geographic divergence is accelerating a broad migration pattern that Census Bureau data has confirmed: Americans are leaving high-cost coastal metros for more affordable Sun Belt and Midwest cities. Phoenix, Nashville, Charlotte, and Austin have absorbed large inflows of price refugees, though those secondary markets are themselves becoming less affordable as a result of the in-migration.

The Investment Property Overhang

Institutional and individual investor ownership of single-family homes is a further complicating factor. A 2026 analysis by the National Association of Home Builders found that investors — ranging from Wall Street-backed single-family rental firms to individual landlords — purchased approximately 22% of all single-family homes sold in 2024, up from 12% in 2012. When investors purchase homes, they reduce the supply available to owner-occupants and can push prices higher through competitive bidding.

The policy response has been varied. Several states have introduced legislation to limit or tax investor purchases of single-family homes, and the Biden administration proposed a tax on single-family rental investors with large portfolios. The effectiveness of these measures in meaningfully improving affordability remains unproven.

The Path Forward

There is no quick fix to a housing affordability crisis that was decades in the making. The most fundamental solution — building significantly more housing in locations where people want to live — faces entrenched political resistance and supply-chain constraints in the construction industry. Meaningful relief likely requires a combination of lower mortgage rates, which depend on Federal Reserve policy and the fiscal situation, zoning reform at the state and local level, and sustained investment in affordable housing production.

For households navigating this market, the data suggests difficult choices: delay homeownership and continue renting, relocate to more affordable geographies, or accept a home that is smaller or further from employment centers than previous generations would have expected at similar income levels. None of these options are satisfying — which is why housing affordability has become one of the most politically potent economic issues of 2026.

Sources: National Association of Realtors, Federal Reserve Bank of St. Louis, Bureau of Labor Statistics, Urban Institute, Federal Housing Finance Agency, Harvard Joint Center for Housing Studies, National Association of Home Builders, Realtor.com, Census Bureau