A credit score is one of the most consequential three-digit numbers in a person’s financial life, influencing not only whether they can access credit but at what price — and increasingly, decisions in employment, insurance, and housing that have nothing directly to do with borrowing. Yet despite credit scores’ pervasive influence, the level of public understanding about how they are calculated, what genuinely improves them, and what is financial mythology is remarkably low. This article examines the data on credit score factors and identifies the actions that actually produce results, separated from the noise.

How FICO Scores Are Actually Calculated

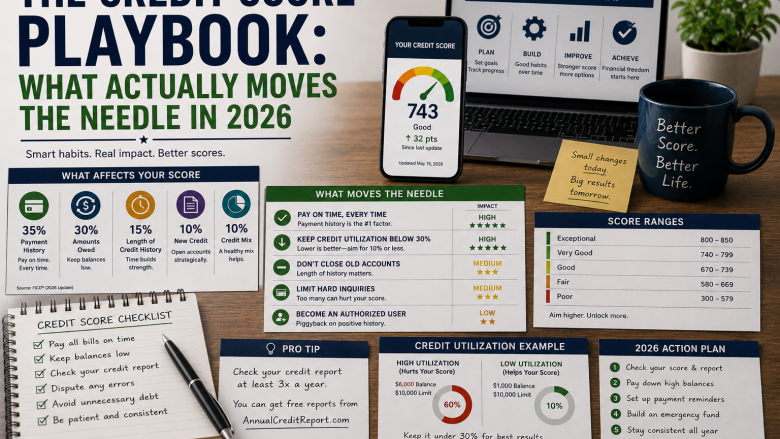

The FICO score — developed by the Fair Isaac Corporation and used in approximately 90% of US lending decisions — is calculated from five factors, each weighted differently. Payment history is the single largest factor at 35% of the score, reflecting whether you have made credit payments on time. Amounts owed — specifically the “credit utilization ratio,” the percentage of available revolving credit you are using — accounts for 30%. Length of credit history (the average age of your accounts) represents 15%. New credit inquiries and recently opened accounts account for 10%. Credit mix — the variety of credit types you hold (credit cards, installment loans, mortgages) — makes up the final 10%.

Understanding these weights immediately clarifies the priority order for credit improvement. Payment history is paramount — a single missed payment, depending on severity and account type, can reduce a FICO score by 60-110 points and remains visible on a credit report for 7 years. Conversely, a perfect payment history across multiple accounts, maintained over years, is the foundation of excellent credit. No other factor comes close in importance.

Credit Utilization: The Most Actionable Short-Term Lever

Credit utilization — the ratio of current credit card balances to total available credit limits — is the most quickly improved credit factor for borrowers with existing credit histories. FICO research shows that the optimal utilization ratio is below 30% across all cards, with scores improving progressively as utilization falls below 30%, 20%, 10%, and approaching zero.

The mechanism is worth understanding: credit bureaus typically receive balance information from card issuers once per month, based on the statement closing date (not the payment due date). A borrower who pays their full balance every month but charges significant amounts may still show high utilization on their credit report if their balance is reported at the time of the statement close. For borrowers approaching an application for a mortgage, car loan, or other significant credit, paying down balances before the reporting date — rather than the due date — can produce a measurable credit score improvement within 30-45 days.

The Experian data shows that the average utilization ratio for FICO scores above 800 is approximately 5.6%, while for scores in the 700-749 range it is approximately 24.7%. This correlation does not imply causation — high-score individuals may carry lower balances because of higher income, not simply better credit behavior — but the directional guidance is clear.

The Length of Credit History Problem — and the Solution

Length of credit history at 15% of the score is the most difficult factor to improve quickly, because it literally requires time. The average age of accounts for FICO scores above 800 is approximately 11.3 years, according to Experian’s most recent State of Credit report. For consumers with thin credit files — recent immigrants, young adults, or those who avoided credit historically — this creates a chicken-and-egg problem: you need credit history to get credit, but you need to get credit to build credit history.

Practical solutions for thin-file consumers include becoming an authorized user on a parent’s or partner’s established credit card account — which adds that account’s history to your credit file, including its age — though this approach requires the primary holder to have good payment history and low utilization. Secured credit cards, backed by a cash deposit equal to the credit limit, provide genuine revolving credit history and are accessible to borrowers with no credit history or damaged credit. Credit builder loans, offered primarily by credit unions and online lenders like Self, create installment loan payment history for consumers who have none.

What Doesn’t Move the Needle (Despite Common Belief)

Several widely circulated beliefs about credit score improvement are simply wrong, and following them can distract from actions that actually matter. Carrying a small balance on credit cards — the advice that “having some balance shows you use credit” — does not improve scores; credit bureaus and FICO models do not reward carrying balances versus paying in full. Closing old credit cards is typically harmful rather than helpful: it reduces total available credit (increasing utilization) and may reduce the average age of accounts (reducing the credit history factor).

Checking your own credit score — a “soft inquiry” — has zero effect on your FICO score. The harmful inquiries are “hard inquiries” from lenders reviewing your file when you apply for new credit. Even hard inquiries have a limited and temporary effect: each hard inquiry reduces scores by approximately 5-10 points and the effect largely disappears within 12 months. Rate shopping for mortgages and auto loans within a focused 14-45 day window is treated as a single inquiry by FICO’s models, enabling consumers to shop for the best terms without score penalty.

The Mortgage Credit Score Reality

For the most financially consequential credit decision most Americans will make — a home mortgage — understanding how lenders use credit scores is particularly important. Most conventional mortgage lenders pull FICO scores from all three major bureaus (Equifax, Experian, and TransUnion) and use the middle score — not the average and not the highest — to determine eligibility and pricing.

The pricing implications of credit score differences are substantial. For a $400,000 30-year fixed mortgage, the difference between a 760+ score (which typically qualifies for the best rates) and a 700-719 score translates to approximately 0.5 percentage points in interest rate — currently the difference between about 6.9% and 7.4% — representing approximately $130 per month in additional payment and over $46,000 in additional interest over the loan life. Understanding and improving credit scores specifically in advance of a mortgage application is one of the highest-return financial actions available to prospective homebuyers.

VantageScore vs. FICO: Knowing Which Score Matters

Many consumers access free credit scores through bank and card websites, credit monitoring services, and apps. The majority of these free scores are VantageScore models rather than FICO scores — a distinction that matters because the two models, while correlated, are not identical and do not always agree on a borrower’s creditworthiness.

VantageScore, developed jointly by the three major credit bureaus, uses a similar 300-850 scale as FICO but weights factors slightly differently and has different data requirements. VantageScore 4.0, the current version, incorporates rental payment history and buy-now-pay-later data that FICO models do not yet include — making VantageScore potentially more favorable for consumers who make timely rent payments but lack traditional credit history.

For practical purposes: when you are applying for significant credit — a mortgage, auto loan, or major credit card — ask the lender specifically which credit score model they will use, and access that specific score before applying. The free scores available from most consumer-facing services are useful monitoring tools but may not precisely reflect what a lender will see.

Credit Repair: What Works and What Is Fraudulent

The credit repair industry is rife with companies that charge substantial fees for services that either don’t work or that consumers can do themselves for free. The FTC receives thousands of complaints annually about credit repair companies that promise to remove accurate negative information from credit reports — something that is both impossible (legally, accurate information cannot be removed before its legal reporting period expires) and fraudulent to promise.

What consumers can legitimately do is dispute inaccurate information on credit reports — a right guaranteed by the Fair Credit Reporting Act. Approximately 25-27% of credit reports contain errors, according to a 2021 FTC study, and some of those errors are consequential enough to affect credit scores. Reviewing your credit reports from all three bureaus — available free weekly at AnnualCreditReport.com under permanent pandemic-era rules — and disputing any inaccurate information with the relevant bureau is a free process that can genuinely improve scores in cases where errors are found.

Sources: Fair Isaac Corporation (FICO) score factor weights, Experian State of Credit 2026, Federal Trade Commission credit report accuracy study, Consumer Financial Protection Bureau, Federal Reserve consumer credit data, FHA and Fannie Mae mortgage pricing grids